Despite there being plenty for investors to consider, the holiday-shortened week ended pretty much where it started. Israel and Iran continued to exchange missile attacks, while global leaders tried to find a resolution to the conflict. President Trump opened the door to diplomacy throughout the week, but on Saturday sent US B2 bombers into Iran and bombed three nuclear facilities. The unprecedented move appears to have materially damaged the facilities and has likely set back Iranian efforts to enrich uranium for a nuclear weapon. It is too early to tell what Iran’s next move will be, but sharp rhetoric from Iran’s supreme leader assures some form of retaliation. This conflict will be at the top of investors’ minds as we enter the new trading week. Interestingly, trade has taken the back seat as we approach the tariff deadline.

The Federal Reserve’s decision to keep its policy rate at 4.25%—4.50% came as no surprise, and Chairman Powell’s press conference did little to move markets. The Fed’s Summary of Economic Projections, updated from March, showed the committee increasing its outlook on inflation and unemployment while decreasing its projections for GDP growth. The Fed now expects PCE to come in at 3% from 2.7% and for the Core reading to increase to 3.1% from 2.8%. Unemployment is expected to rise from 4.5% to 4.4%. GDP growth is expected to fall from 1.4% to 1.7%. The Fed still projects two twenty-five basis point cuts in 2025, with the market expecting the first cut in September. Notably, the Bank of Japan and Bank of England kept their policy rates at 0.50% and 4.25%, respectively.

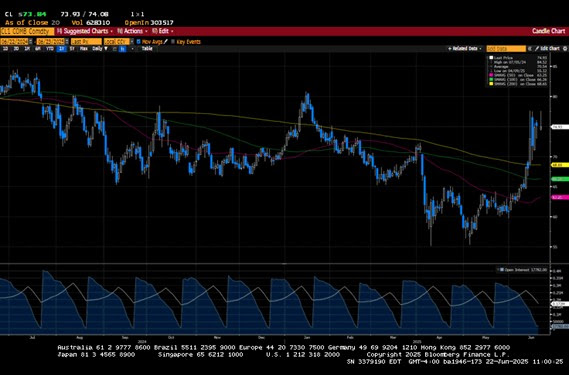

The S&P 500 fell 0.2%, the Dow closed unchanged, the NASDAQ increased by 0.2%, and the Russell 2000 rose 0.4%. US Treasuries advanced across the curve. The 2-year yield fell by five basis points to close the week at 3.91%, while the 10-year yield declined by four basis points to close at 4.38%. Oil prices were volatile again, but they finished the week higher by only $0.67, closing at $73.83 a barrel. Oil is likely to have a significant bid to it once it opens. Some are calling for it to trade above $80 a barrel. Gold prices fell by 1.9% or $66.50 to close at $3385.80 per Oz. Copper prices were little changed at $4.83 per Lb. Bitcoin dropped to $100,000, down about $4,500 from the prior week. The US Dollar index had a 0.6% advance, closing the week at 98.70.

The economic calendar was pretty quiet. June Retail Sales were weaker than expected, coming in at -0.9% versus the estimate of -0.6%. The Ex-auto reading came in at -0.3% versus the forecast of 0.1%. Initial Claims fell by 5k to 245k, while Continuing Claims fell by 6k to 1945k. Housing Starts and Building Permits came in much weaker than expected. Housing Starts came in at 1256k versus 1356k, while Building Permits came in at 1393k versus the consensus of 1411k.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involve risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.